Press release

10.08.2023

Liquid alternatives in the first half of 2023: significant outflows continue despite positive performance

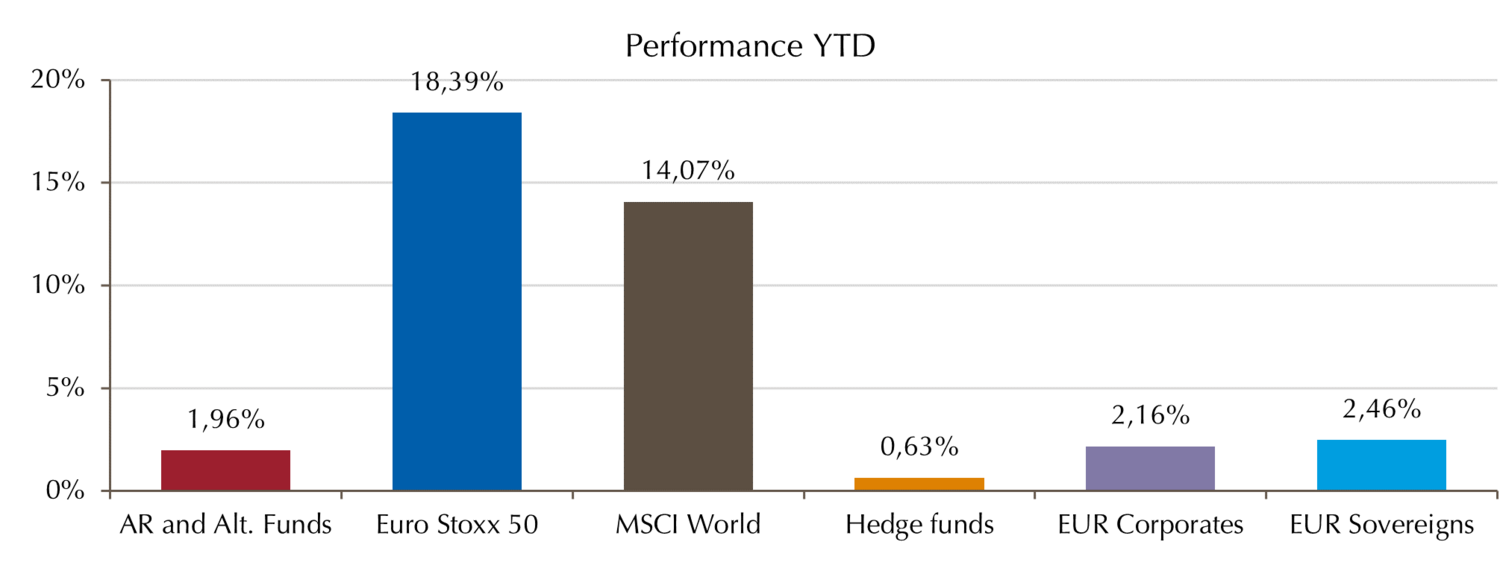

Investors have been withdrawing from UCITS-compliant hedge fund strategies ever since the rapid turnaround in interest rates. Outflows accelerated in the first half of the year compared to 2022, totalling EUR 19.4 billion as of 30 June 2023. Amid a generally positive market environment, this asset class outperformed unregulated hedge funds, remained roughly on a par with bonds and lagged behind equities at 1.96%. The low volatility of this asset class means it is proving its worth as a stabilising portfolio component in the medium term.

The withdrawal of investor capital reinforces a trend that has been evident since 2022, with outflows exceeding the total for the entire previous year (EUR -17.6 billion) in the first half of 2023. As a result, the market volume has fallen by 8% to just under EUR 242 billion. Statistics from the Deutsche Bundesbank show where this withdrawn capital is going. In its latest press release on the acquisition of financial assets, the Bundesbank highlights the “historically high reallocations” to fixed-income investments and bonds during the first quarter. It is clear that the new interest rate environment and economic uncertainty are both influencing current investor behaviour.

“Increased interest rates are currently making liquid alternatives less attractive in the eyes of many investors,” said Ralf Lochmüller, Managing Partner and CEO of Lupus alpha. “At -4.3%, however, institutional volumes have only fallen by half as much as the evaluated segment as a whole. This suggests that institutional investors, in contrast to retail investors, have already largely finished reallocating funds away from regulated hedge fund strategies,” Lochmüller added.

Above-average returns possible with careful manager selection

With an average performance of 1.96%, liquid alternatives were unable to keep pace with the major international equity indices. However, a closer look at individual strategies and funds confirms that investors were able to achieve above-average returns by selecting the best funds. Experience shows that the return differential between funds can be considerable, even within individual strategies. For example, while the Alternative Long/Short Equity strategy generated an average return of 2.2%, the best funds in this group achieved 20%. Careful manager selection can produce extremely good results in this market.

Performance in the first half of 2023: lagging behind equities and bonds but ahead of unregulated hedge funds

×

![]()

The liquid alternatives asset class is proving its worth as a diversifying portfolio component in the medium term. Most strategies deliver impressive performance over a five-year period by recording low volatility compared to equities of between 5% and 15%, a feat achieved by both fixed-income and other strategies. At the same time, liquid alternatives have often saved their investors from painful drawdowns, with almost three-quarters of these funds limiting their maximum losses to 20% over the past five years despite the coronavirus crisis and war in Ukraine.

Ralf Lochmüller: “These stabilising characteristics are barely registering with investors in the current market environment, even though 2022 showed that bonds do not provide any additional security per se. As a result, alternative investment concepts that have little correlation with the broader equity markets provide a route to a more stable portfolio in the long term – even in the new interest rate environment.”

Download the press release

About the Study

Since 2008, Lupus alpha has been evaluating the universe of absolute return and liquid alternatives funds on the basis of data from Refinitiv. The Study covers UCITS-compliant funds with an active management approach that are authorised for distribution in Germany. The Study focuses on market size, development and composition, performance in the investment segment and individual strategies, as well as key risk figures. It evaluates the three levels of aggregation – the overall universe, strategies within the universe, and funds within the strategies – and distinguishes between 14 strategies. Long Short Equity, for example, consists of 108 funds.

About Lupus alpha

As an independent, owner-operated asset management company, Lupus alpha has been synonymous with innovative, specialised investment solutions for more than 20 years. As one of Germany’s European small and mid-cap pioneers, Lupus alpha is one of the leading providers of volatility strategies as well as collateralised loan obligations (CLOs). Global convertible bond strategies complete its specialised product range. The Company manages a volume of approximately EUR 14.0 billion for institutional and wholesale investors. For further information, visit www.lupusalpha.de.